Many people are asking: Should I buy a house in the UK now? The market feels uncertain. House prices can change. Mortgage rates can move up or down. Renting can also feel expensive, so buying starts to look more appealing.

At the same time, buying a home is a big decision. You do not want to rush into it without thinking about your money, your job, and your long-term plans.

Is Now a Good Time to Buy a House in the UK?

Current UK Housing Market Overview

The UK housing market is always changing. In some areas, UK property prices may be rising slowly, while in others they may be flat or even falling. This means location matters a lot.

Supply and demand also play a big role. If there are fewer luxury homes for sale, prices can stay high. If more homes come to market, buyers may have more choice and more room to negotiate.

Regional differences are important too. London, the South East, the Midlands, and northern areas often behave differently. So when people ask, “Should I buy a house now in the UK?” the best answer is often, “It depends on where you want to live.”

What Experts Are Saying

Many experts believe the market is more balanced than it was during the hottest years of price growth. That does not mean prices will crash. It simply means buyers may have more room to think and compare.

Buyer confidence can improve as mortgage rates stabilise and wages keep pace with costs. But confidence is not the same as certainty. The best move is to focus on what you can afford, not just on market headlines.

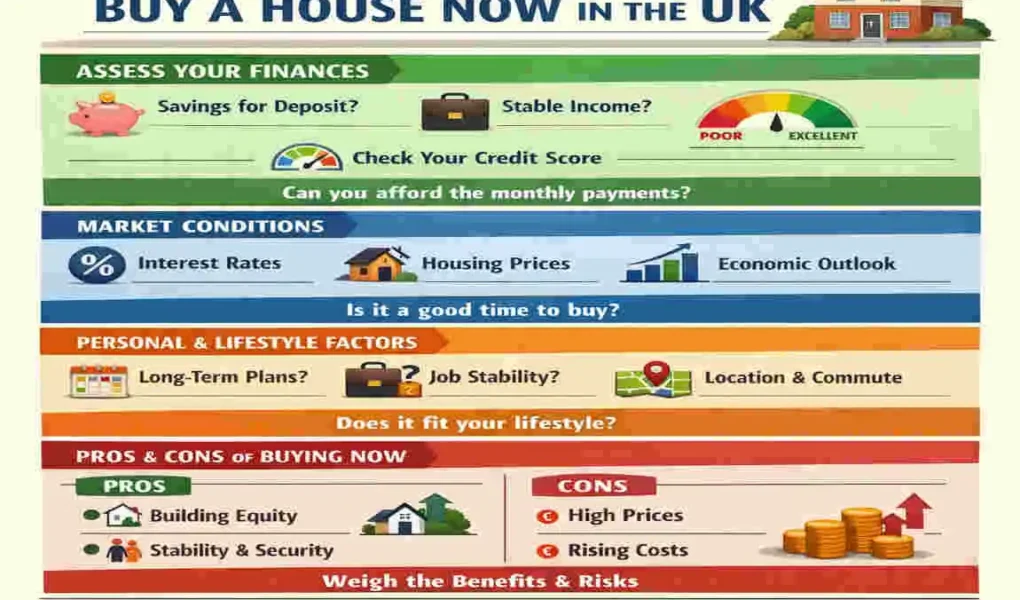

Factors to Consider Before Buying a House

Your Financial Situation

Before buying a house in the UK, look closely at your income. Is it stable? Do you expect any major changes soon? If your job is secure and your earnings are reliable, buying may feel safer.

Savings matter too. You will need money not just for a deposit, but also for fees, moving costs, and the first few months of ownership. It is also wise to keep an emergency fund for surprise costs.

Mortgage Interest Rates

UK mortgage rates affect how much you pay every month. Even a small rate change can make a big difference over time.

A fixed-rate mortgage gives you predictable payments for a set period. A variable rate can move up or down, which may be risky if your budget is tight. If you want peace of mind, a fixed deal may suit you better.

Deposit Requirements

Most buyers need a deposit. In many cases, the minimum is around 5% of the property price, though a larger deposit can open better deals.

A bigger deposit can help in two ways. First, it may lower your monthly payments. Second, it can improve the mortgage offers you receive. This is especially useful for a first-time buyer in the UK trying to keep costs under control.

Monthly Budget

Do not focus only on the mortgage. A home comes with many ongoing costs.

Here are the main ones to include in your budget:

- Mortgage payments

- Council tax

- Utilities

- Home insurance

- Maintenance and repairs

If these costs feel too tight, it may be better to wait. A home should give you stability, not constant money stress.

Pros of Buying a House Now in the UK

Start Building Equity

When you buy, your monthly payments help you own part of the property. This is called equity. Over time, this can feel better than paying rent, where the money does not come back to you.

Greater Property Choice

In some markets, buyers have more choice now than they did before. More choice can mean less pressure and more time to compare modern homes properly.

Protection Against Rising Rent

Rents in the UK can rise over time. Buying may protect you from future rent increases, especially if you plan to stay in the same home for many years.

Long-Term Investment Potential

A luxury home is not just a place to live. It can also be part of your financial future. If property values rise over the long term, you may benefit when you sell later.

Reasons to Wait Before Buying

High Mortgage Rates

If rates are high, borrowing becomes more expensive. That can make monthly payments harder to manage, especially for first-time buyers.

Limited Savings

If you barely have enough for the deposit and fees, buying now may be risky. You need a cushion for repairs, moving, and emergencies.

Job Uncertainty

If your income is not stable, a mortgage can create pressure. Losing a job or changing careers can make homeownership stressful.

Falling House Prices in Some Areas

Some local markets may be weaker than others. If prices are falling in the area you want, waiting could make sense. It may also give you more time to watch the market.

Who Should Buy a House Now?

First-Time Buyers

A first-time buyer in the UK with a stable income, solid savings, and a long-term plan may be ready to buy now. If you are tired of rising rent and want a place of your own, this could be the right time.

Families Needing More Space

If your family is growing, waiting may not help. Sometimes the need for more space is more important than trying to time the market perfectly.

Long-Term Homeowners

If you plan to stay for five years or more, short-term price changes matter less. Over a longer period, buying can become more attractive.

Investors

People buying for rental income or future profit need to study the market carefully. For investors, local demand, mortgage costs, and rental yields matter a lot.

Who Should Delay Buying?

Some people are better off waiting. If your income is unstable, your savings are low, or you have a lot of debt, it may be safer to pause.

You should also delay if you plan to move again soon. Buying and selling in a short period can be expensive. If you are unsure about the area, your job, or your plans, renting a little longer may be wiser.

Tips to Make the Right Buying Decision

Check Your Credit Score

A strong credit score can improve your chances of getting a mortgage. If your score is weak, work on improving it before you apply.

Compare Mortgage Deals

Do not accept the first offer you see. Compare rates, fees, and repayment terms. Small differences can save you a lot over time.

Research Local Property Markets

Look at the area you want to buy in. Check recent prices, demand, and how long homes stay on the market. Local knowledge matters more than national headlines.

Calculate Total Ownership Costs

Think beyond the asking price. Add in stamp duty, legal fees, surveys, insurance, bills, and repair costs. This gives you a more realistic picture.

Speak With a Mortgage Adviser

A mortgage adviser can help you understand what you can borrow and what kind of deal may suit you best. This is especially helpful if you are a first-time buyer.

Common Mistakes to Avoid

Buying Beyond Your Budget

This is one of the biggest mistakes. Just because a lender approves a certain amount does not mean you should borrow it all.

Ignoring Hidden Costs

Many buyers forget fees, maintenance, and bills. These costs can stretch your budget fast.

Skipping Surveys

A survey can uncover problems that are not easy to see. It may save you from costly surprises later.

Not Comparing Lenders

Mortgage deals vary a lot. Always compare before you commit.

Making Emotional Decisions

It is easy to fall in love with a house. But try to stay practical. A good home should also be a good financial fit.

FAQ

Should I buy a house in the UK now or wait?

If you have a stable income, savings, and a long-term plan, buying now may work well. If your finances feel tight, waiting could be safer.

How much deposit do I need to buy a house in the UK?

Many buyers need at least 5%, but a larger deposit often gives better mortgage options and lower monthly payments.

Are UK house prices expected to fall?

Some areas may soften, while others stay steady. The UK housing market often moves differently by region.

What salary do I need to buy a house in the UK?

It depends on the property’s price, your deposit, debts, and the lender’s rules. A mortgage adviser can help you estimate this more accurately.

Is renting cheaper than buying in the UK?

Sometimes renting is cheaper in the short term, but buying may be better long term. It depends on rent levels, mortgage rates, and how long you stay.

| Factor | What to Consider | Why It Matters |

|---|---|---|

| Financial Readiness | Check your savings, income, and monthly budget. | Ensures you can afford mortgage payments and other costs. |

| Mortgage Rates | Compare current UK mortgage interest rates. | Lower rates reduce long-term borrowing costs. |

| House Prices | Research local property prices and market trends. | Helps determine if prices are fair or likely to change. |

| Deposit Size | Aim for a larger deposit if possible (typically 10–20%). | A bigger deposit can secure better mortgage deals. |

| Job Stability | Consider the security of your employment and income. | Stable finances reduce the risk of missed payments. |

| Long-Term Plans | Decide if you plan to stay in the property for at least 5 years. | Buying is generally more cost-effective over the long term. |

| Monthly Costs | Include mortgage, council tax, insurance, utilities, and maintenance. | Prevents unexpected financial pressure. |

| Credit Score | Review and improve your credit history before applying. | A higher credit score can improve mortgage approval chances. |

| Local Market Conditions | Assess demand, supply, and future development in the area. | Affects property value and investment potential. |

| Professional Advice | Speak with a mortgage adviser or financial expert. | Helps you choose the most suitable mortgage and buying strategy. |